Survival of the fittest in the luxury digital economy

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

Digital is a vital source of growth for the luxury industry and a powerful way to develop brand equity. According to consulting firm McKinsey, a “Luxury 4.0” model is taking shape. Who will survive and who will become extinct?

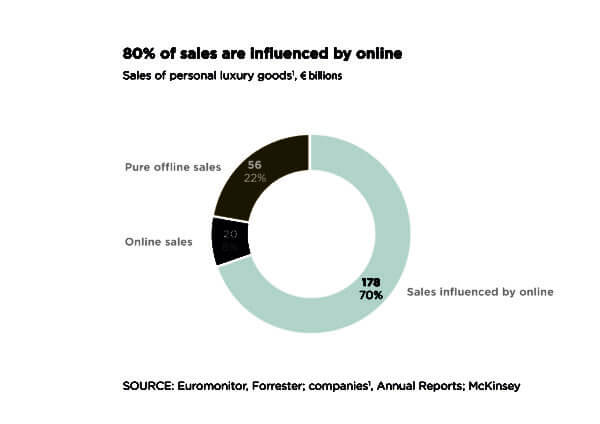

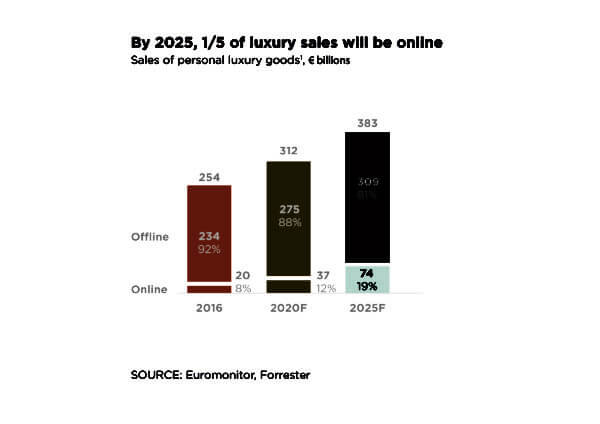

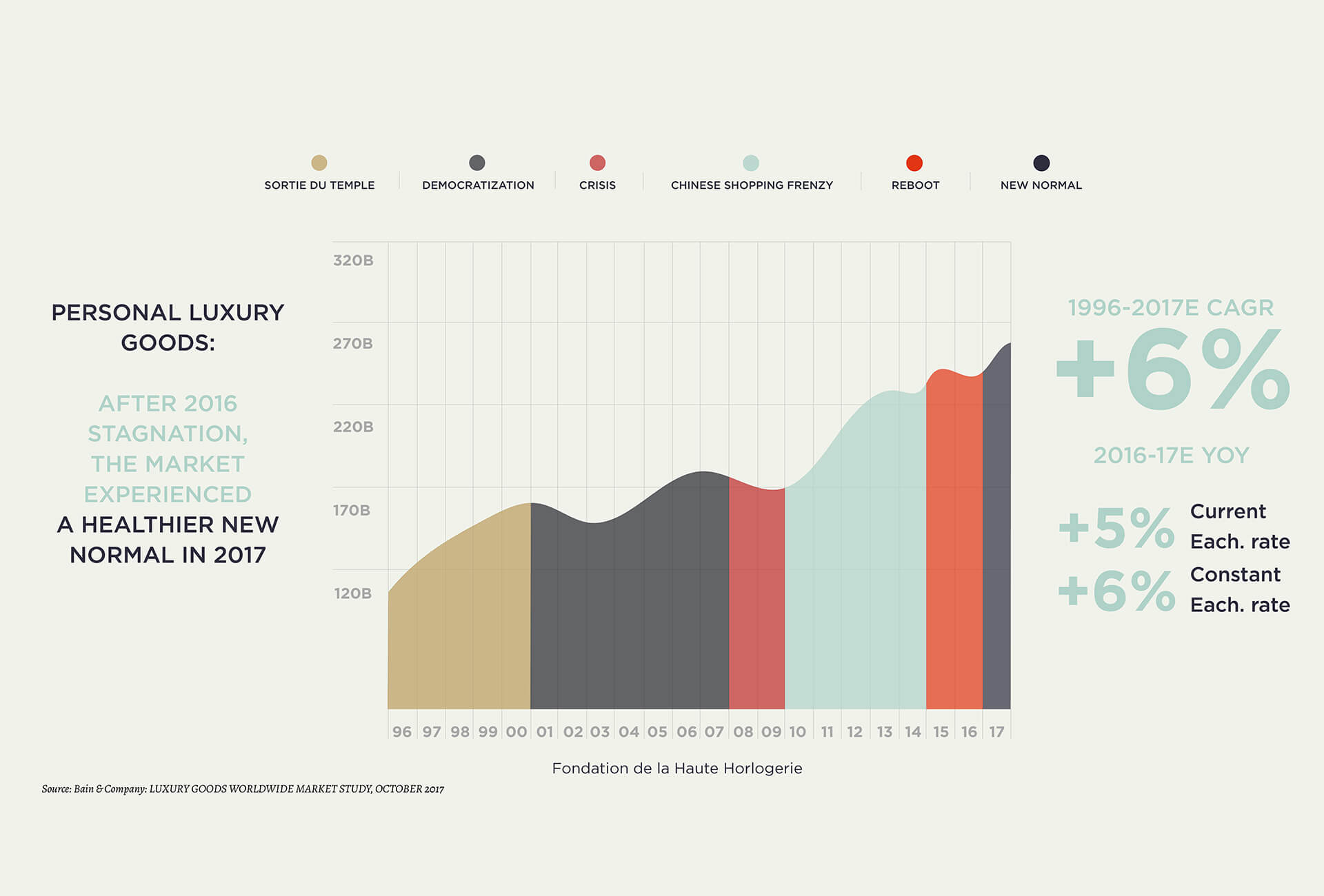

Much has been written about Darwin’s theory of natural selection, refuted in certain countries on religious grounds. Consulting firm McKinsey hasn’t yet investigated evolutionary theory, but has borrowed the principle put forward by Charles Darwin (1809-1882) to describe a situation whereby only those luxury brands that adapt to digital disruption will survive. “Digital Darwinism”* is a reality that brands ignore at their peril. A few figures for the doubters: online sales of personal luxury goods have increased five-fold from 2009 and accounted for 8% of the €254 billion global luxury market in 2016. They are expected to more than triple by 2025 to around €74 billion (19% of total luxury sales). Better still, nearly 80% of luxury sales today are digitally influenced – only a fifth of luxury shoppers begin and end their customer journey without any contact with the web.

Multiple touchpoints

As McKinsey notes, digital is more than a question of generation. When analysing online luxury shopping habits, millennials come out tops as expected, but baby boomers (50 years-plus) aren’t far behind in terms of mobile device ownership and internet use. These same mobile devices are replacing desktop connections as the preferred means of accessing information and making a purchase which, as McKinsey explains, “poses additional challenges for brands: how do you convey your dream and translate the magic of your story-telling to a 10cm by 6cm screen? How do you show the breadth of your collection and the richness of its details to a consumer who is in an elevator or on a noisy city street?”.

The linear customer journey has been blown to bits. Today’s luxury shopper engages with brands via multiple touchpoints – as many as 15 in the case of Chinese luxury consumers – and at least half of these are digital. Brands must deliver a seamless and coherent message and image across these touchpoints, wherever they are, particularly now that digital luxury is increasingly a customer-to-customer (C2C) economy. “The consumer is central to the shopping journey, from advocacy to sales,” says the study. “Luxury consumers are highly engaged on social media and are moving from being paying observers of the show to being actors on stage.” Again, the question brands must answer is how to turn consumers into ambassadors for their products, knowing that it only takes one click to turn a “like” into a “hate”. According to McKinsey, luxury firms must “learn to deal with ambiguity and accept that some aspects of their messaging will be cocreated with their customers rather than controlled unilaterally by their management team.”

The era of contextual marketing has begun

How have brands responded? Not all in the same way, according to McKinsey, which has analysed how budgets are allocated between print, digital and events – with important synergies to be made between the latter two. Omega, for example, spent 10% to 15% of its 2016 marketing investment on events and 25% on digital. Print continued to account for between 60% and 65%. The spread is similar at Cartier and Bulgari, whereas Burberry makes it an even split. So who is winning the “e-rush”? Monobrand sites continue to take the lion’s share with almost €5 billion of online luxury sales in 2016. However, at 20%, their compound annual growth rate (CAGR) 2014-2016 is only half that of multibrand marketplaces such as Lyst.com or Farfetch.com that are better able to satisfy customers for whom choice matters.

McKinsey’s analysis shows that digital’s growing penetration of the luxury market has an impact on three levels, for the most forward-looking brands at least. They are digitising their business to build a “Luxury 4.0” model that is faster and more agile. They are also using big data to develop a more relevant understanding of consumer behaviour, with the aim of proposing customised products and services. The study tells the story of the early days of luxury, when Louis Vuitton would send handwritten letters to customers with recommendations for particular travel bags for a transatlantic journey to New York. In today’s language, this translates into contextual marketing for the ultimate luxury experience. Some brands have enlisted the help of the digital giants – Burberry and Google, for example – to create a luxury ecosystem… where only the fittest will survive?

*Apparel, Fashion & Luxury Group – The age of digital Darwinism

Enhance the customer experience and transform your business to survive and prosper in the luxury digital era. McKinsey & Company, January 2018.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}