Swiss watch exports grew 2.7% in 2017

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

Strongest growth was recorded in the second half, when shipments increased almost 5%. For the full twelve months, Hong Kong (+6%) and China (+18.8%) set the pace. The major luxury groups are also on the up and up. Richemont, LVMH and Swatch Group have all announced significantly stronger results.

There wasn’t much in the way of suspense. By the second half of 2017, it was already clear that the Swiss watch industry was back on track after two lean years. Data just released by the Federation of the Swiss Watch Industry (FH) now puts a figure on this upswing, already evident in January during the Salon International de la Haute Horlogerie in Geneva. For the entire year, shipments rose by 2.7% to CHF 19.9 billion. As the Federation notes, “the trend stabilized in the first half (+0.3%), while the second saw substantial growth (+4.9%).” And as one good thing leads to another, “development of digital communication and distribution channels and the types of consumption favoured by the millennials will be priorities in 2018. In this context, watch industry export growth is likely to be comparable to that observed in 2017.”

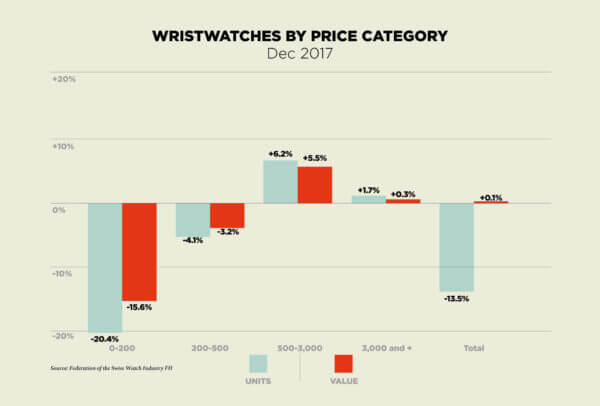

The number of units exported continued to fall, dropping 1.1 million (-4.3%) to 24.3 million. Most of this decline came from quartz watches. Conversely, mechanical watches are performing well. They grew in both value (+4.6%) and number of units (+3.9%). Growth was driven by watches above CHF 200 (export price) and by steel watches. Geographically speaking, the sharpest recovery came from Asia (+4.8%), which generated half of all export sales last year, ahead of Europe (+2.6%). In contrast, shipments to the United States fell for the third consecutive year (-4.4%), which dampened the American continent overall (-2.7%). In terms of individual markets, Hong Kong held up well (+6%) and moreso China (+18.8%), respectively the number-one and number-three destinations for Swiss watches.

Luxury is back in business

This upswing in activity is mirrored by performance from the sector’s main players. Richemont set the ball rolling when it published its nine-month results to end December, up 7% to €8,724 billion. Now Swatch Group confirms this positive trend. At current exchange rates, the world’s biggest watch group reported an increase in net sales of 5.4% to CHF 7,960 billion. This progression was even greater in the Watches & Jewelry segment (excluding Production), where sales increased by 6.9% with a marked acceleration of 12.2% in the second half. To top it all, December recorded the second best monthly sales in the group’s history. These figures are confirmed by the overall operating result, which climbed 24.5% to CHF 1 billion. Year-on-year, operating margin grew from 10.7% to 12.6%. Of the 20 brands in the group, Harry Winston is credited with “extraordinary performance”, while the Prestige & Luxury segment surpassed the other segments in terms of growth. Looking ahead, Longines is expected to achieve sales of CHF 2 billion in the medium term, while Tissot is already making over CHF 1 billion.

LVMH, the world’s leading luxury conglomerate, reports a record year in 2017. The group recorded a 13% leap in revenue to €42.6 billion. Profit from recurring operations came to €8.3 billion (+18%). With the exception of Wines & Spirits, every segment posted double-digit organic growth. This of course includes Watches & Jewelry, where revenue increased 10% to €3.8 billion and profit from recurring operations reached €512 million (+12%). Bulgari continued to gain market share while TAG Heuer and Hublot reported further growth. The one cloud in the sky came from Zenith. Still putting its house in order, the brand was conspicuous by its absence in the breakdown of the different brands’ performance. Given the brighter business context, it could just be a matter of time.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}