The luxury market returns to “healthy” growth

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

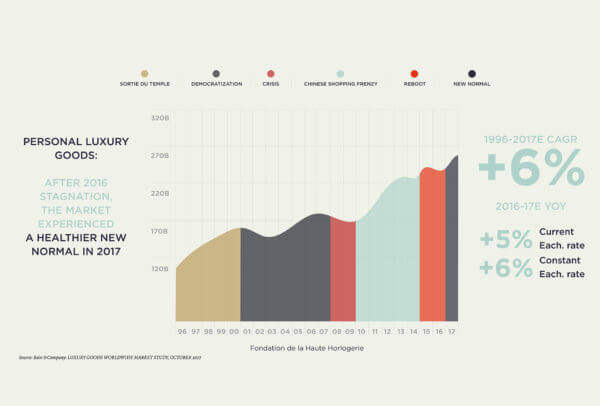

The latest study from Bain & Company consulting firm is decidedly optimistic. After stagnation in 2016, normality returns to the overall luxury market which grew by 5% in 2017 to reach an estimated €1.2 trillion globally.

With Christmas almost upon us, Bain & Company adds to the festive cheer with a sackful of good news. The first, and probably most important, is the announcement of a return to healthy growth for the overall luxury market. We all remember the golden years of 2009 to 2015, when Chinese consumers splurged on personal luxury goods, which include fine watches, and the market cumulatively increased by 65% from €153 to €251 billion, according to Bain & Company figures. No less vivid is the sting of the slump, not least for the Swiss watch industry whose exports tumbled 10% in 2016. Adding its voice to the general sentiment that measured growth is the most likely option, the consulting firm expects the luxury market to grow by 5% in 2017 to an estimated €1.2 trillion globally. This aligns with the sector’s long-term potential, with annual growth forecast to continue by 4% to 5% in the next three years, particularly for personal luxury goods.

Local consumption picks up

This “healthy” evolution reflects a shift in balance across the market’s essential components. Sales have picked up the most speed among the now inevitable Millennials. They account for 38% of luxury buyers, and brands have little choice than to adapt their strategy to this discerning clientele. Another factor that has helped stabilise the market has been the emergence of local consumption as a driver for growth. This is particularly apparent in Asia, and specifically in China (where watch exports climbed 17.3% between January and October this year), but is also noticeable in Europe and the United States. Tourist flows have continued to support the market, especially in Europe and specifically in the UK which has benefited from sterling’s weakness. Lastly and just as significantly, growth is being driven by increases in volumes rather than by artificial price increases, which can prove a dangerous strategy when the market hits a soft patch.

Online sales still climbing

This new face of the global luxury market is matched by a change in distribution channels. According to Bain & Company, the sector is evolving into an ecosystem of different channels with the internet destined to play a major role. According to the firm’s figures, online sales grew by an average 25% a year between 2013 and 2016, and jumped by 24% in 2017 to €23 billion – only 11% of which concerns hard luxury which includes fine watches. Online sales are now spread fairly equally across brands themselves (31%), traditional retailers that also have an online presence (30%) and, taking the largest share, e-tailers (39%). There can be no more eggs-in-one-basket. Instead, distribution strategies must extend across virtual and physical, own-name and multibrand, travel retail, flagship stores, even off-price… bearing in mind that by 2020 an estimated quarter of sales will be made online. In which case the number of monobrand stores (currently around 20,000 worldwide) is unlikely to increase by any great amount. This is one way for brands to maintain operating margins at the same generous level – estimated by Bain & Company at an average of 19% for a year that is clearly ending on a positive note.

{kind=link}

{kind=link}