The Swiss watch industry is bursting at the seams

close

Christophe Roulet

Editor-in-chief, HH Journal

CLOSE

T

With exports growing 16% last year to almost CHF 16 billion and a further 23% in January 2008, the Swiss watch industry, if we needed reminding, is hot property. Were we to look only at Fine Watches, the market goes from hot to boiling-point, gaining 25.3% in value terms over the twelve months of 2007 to reach CHF 7.83 billion (up 16.7% in volume terms), and almost 40% for the first month of 2008 (+45% in volume), according to statistics published by the Federation of the Swiss Watch Industry.

With such a rate of growth, with a clear acceleration over the last two years, what were viable criteria when organising production ten years ago are now quite simply out of the question, for one obvious reason: the entire value-creation chain is set to burst, the biggest problems being serious bottlenecks in production leading to ever-longer delivery times, a shortage of skilled labour and major shortfalls in the quality of parts. “We need to bring the situation under control which means shorter waiting times,” commented Luigi Macaluso, Chairman of the Sowind group (Girard-Perregaux and JeanRichard) recently.

Sights trained on suppliers

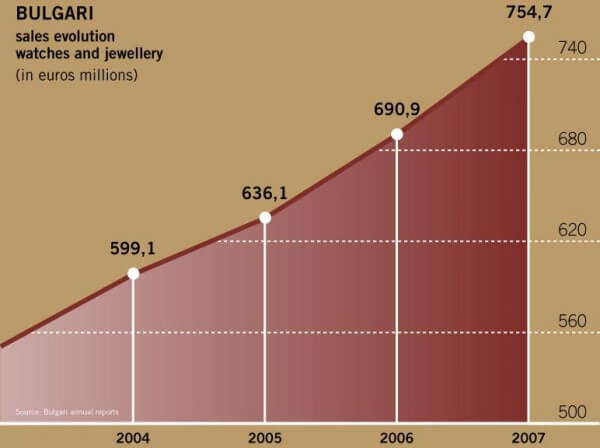

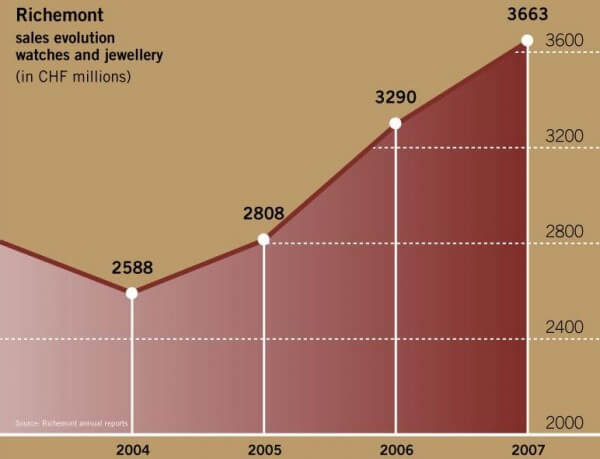

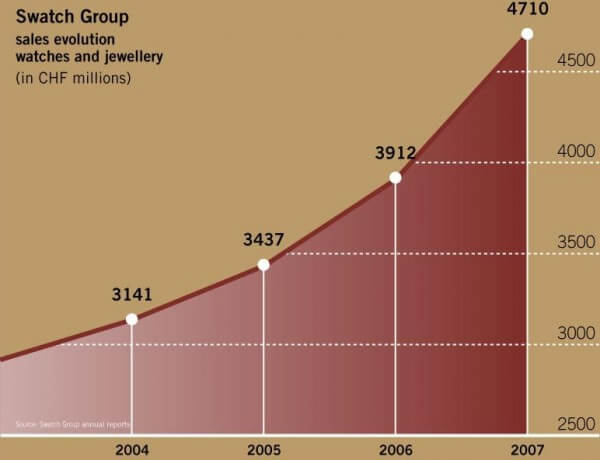

For the watch groups that sailed through the 2007 financial year, as figures show at Swatch (2007 sales up 17.6%), LVMH (organic revenues growth of 19% for Watches & Jewelry), PPR (results for its luxury division up 29%) and Richemont (third-quarter sales up 14% at constant exchange rates), this “mad surge” in sales raises a number of questions, mostly concerning production. With good cause. In the 1990s, these luxury multinationals went shopping for prestigious brands, sparking an unprecedented wave of mergers and acquisitions in the branch. But as the experts like to remind us, while the brand is a unique gateway to the customer, the products still have to meet expectations.

And so watchmakers started casting an eye towards their suppliers, intent on honing their industrial resources as part of sweeping vertical integration. While these buy-outs of small and medium firms may not have made headline news in the same way the take-over of Jaeger-LeCoultre, Breguet or Zenith once did, they still caused a subtle but nonetheless important shift in the watchmaking landscape. Since the early 2000s, numerous suppliers of dials, hands, cases and movement parts have changed owners, swelling the ranks of already well-established firms as well as others eager to develop industrial resources worthy of the name, the ones that strive towards that holy of holies, the Manufacture movement. Clearly we haven’t seen the last of these take-overs of highly-specialised small and medium enterprises, as illustrated these past six months by the acquisition of Elinor, a manufacturer of precious metal cases, by F.P. Journe, of Donzé-Baume, a specialist in cases and bracelets, by Richemont, of Indexor, a manufacturer of hour markers, by Swatch via MOM Le Prélet, and the alliance between Bulgari and Leschot, another case-maker. Still, companies realised quite some time ago that vertical integration alone was no longer sufficient…

A spontaneous generation of new workshops

Expertise is one thing, production capacity is another. Some companies are so cruelly lacking capacity that delivery times for certain new products can stretch to as much as three years. Once again, the most comfortable remedy has been to hunt down an easy target, or even to form an alliance with one of the watchmakers working behind-the-scenes, making high-end movements for third parties. This was the route chosen recently by Hermès when it acquired a 25% stake in Vaucher Manufacture Fleurier. Richemont had the same goal in mind when it took over Minerva and production facilities at Roger Dubuis. As for Bovet, by reviving Dimier it has simply given a prestigious new name to STT Holding, a recent acquisition comprising three specialised manufacturers of tourbillons, balance-springs and calibres.

Once again though, this shuffles the deck but doesn’t add any new cards to a sector which, overall, needs to extend its production facilities. No sooner said than done; companies have got the message and are busy composing the architectural masterpieces that will give them more production space. The same phenomenon is at work among suppliers too. “Bricks-and-mortar investments by companies in the watch sector have multiplied during this upswing,” observed Nicola Thibaudeau, CEO of MPS Micro Precision Systems SA, recently. “In the vale of Saint-Imier in the Franches-Montagnes district as elsewhere, over the past few years every village has seen one or more buildings spring up and new workshops and machines move in. What will become of these investments when the cycle enters a downturn?” For the moment, this isn’t something the sector seems too concerned about!